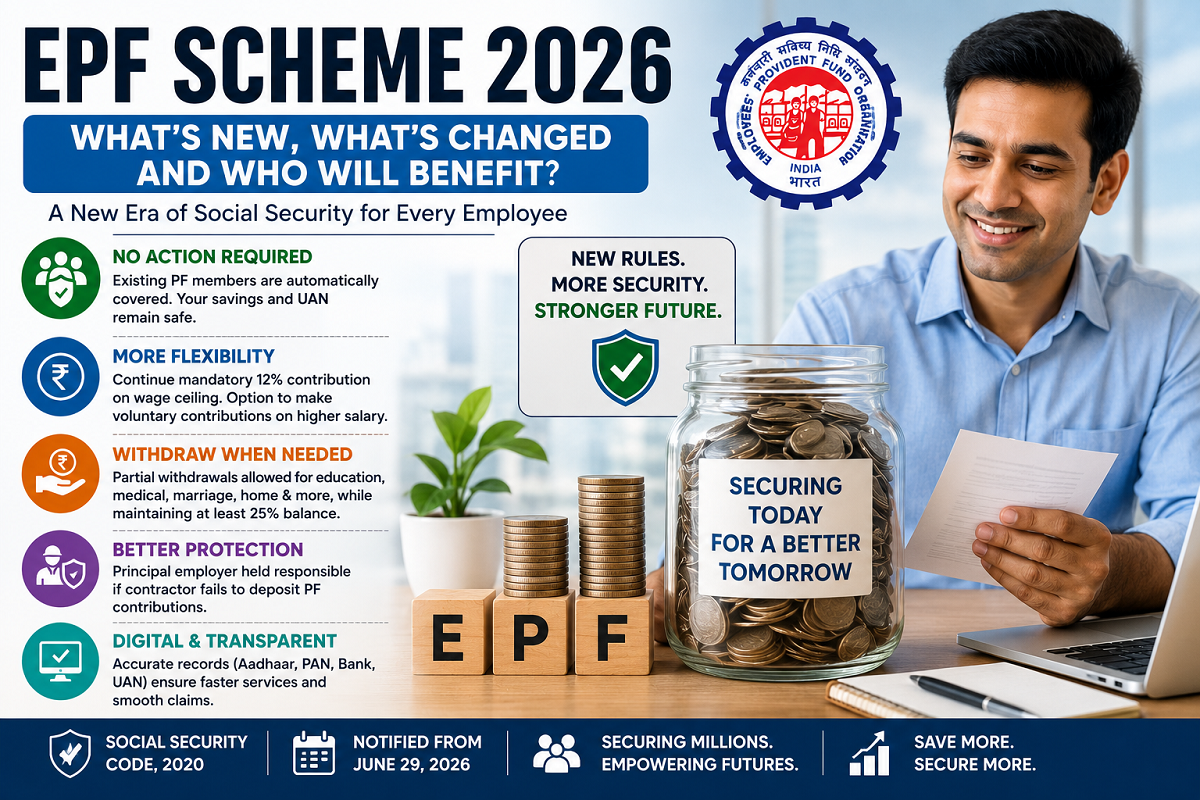

The Government of India has officially introduced the Employees' Provident Funds (EPF) Scheme, 2026 under the Code on Social Security, 2020, replacing the long-standing EPF Scheme, 1952. Alongside it, the government has also notified the Employees' Pension Scheme (EPS) 2026 and the Employees' Deposit-Linked Insurance (EDLI) Scheme 2026.

While the new framework modernizes India's provident fund system, it does not require existing EPF members to open new accounts or transfer their savings. Instead, the scheme aims to improve flexibility, simplify compliance, strengthen digital services, and enhance social security for employees, including contract workers.

Here's a detailed look at the key changes introduced under EPF Scheme 2026.

Existing PF Members Do Not Need to Take Any Action

One of the biggest concerns among employees has been whether the introduction of EPF Scheme 2026 would affect their existing provident fund accounts.

According to the notified scheme, employees who are already members under the EPF Scheme, 1952 will automatically become members of the new scheme. Their Universal Account Number (UAN), accumulated PF balance, and membership status will continue without interruption.

In other words:

- Existing PF accounts remain valid.

- Accumulated savings remain protected.

- No fresh registration is required.

The provisions relating to Excluded Employees also continue under the new framework. Employees whose salary exceeds the prescribed wage ceiling at the time they join employment will remain outside mandatory EPF coverage unless covered under applicable rules.

Mandatory Contribution Remains the Same

The basic contribution structure has not changed.

Both the employee and the employer will continue contributing 12% of eligible wages towards the provident fund, subject to the applicable wage ceiling.

At present, with the wage ceiling of ₹15,000 per month, the mandatory EPF contribution remains:

- Employee contribution: ₹1,800 per month

- Employer contribution: ₹1,800 per month

More Flexibility Through Voluntary Contributions

One of the notable additions in EPF Scheme 2026 is greater flexibility for voluntary contributions.

Employees who wish to build a larger retirement corpus can voluntarily contribute on wages exceeding the statutory wage ceiling.

The scheme also permits employers, if they choose, to match these additional voluntary contributions.

Importantly, employees can later reduce or discontinue the voluntary portion based on their financial circumstances, making retirement planning more flexible than before.

Example

If an employee earns ₹80,000 per month, mandatory EPF contributions will still be calculated on the statutory wage ceiling unless higher contributions are opted for.

The employee may voluntarily contribute on the entire salary to accumulate higher retirement savings. If financial commitments increase later—for example, after taking a home loan—the employee can reduce or stop the additional voluntary contribution while continuing the mandatory contribution.

Partial Withdrawals Continue for Eligible Needs

EPF Scheme 2026 retains the existing provisions allowing withdrawals for specified purposes.

Eligible members may continue to withdraw funds for situations such as:

- Medical treatment

- Higher education

- Marriage

- Purchase or construction of a house

- Retirement

- Permanent settlement abroad

- Employment outside India

However, the new scheme emphasizes maintaining a minimum balance in the account.

According to the notified provisions, members are generally expected to retain at least 25% of their total accumulated contribution, ensuring that adequate retirement savings remain available after partial withdrawals, subject to the applicable withdrawal rules.

Greater Protection for Contract Workers

The revised scheme also strengthens safeguards for employees engaged through contractors.

If a contractor fails to deposit EPF contributions or is not properly registered, the Principal Employer will remain responsible for ensuring that provident fund contributions are deposited.

This provision is intended to improve compliance and better protect the social security rights of contract workers across various industries.

Digital Records Become More Important

EPF Scheme 2026 places increased emphasis on maintaining accurate digital records.

Employees are expected to ensure that important details remain updated, including:

- Aadhaar

- PAN

- Aadhaar-linked bank account

- Universal Account Number (UAN)

Keeping these records current is expected to facilitate:

- Faster claim settlements

- Smooth PF account transfers

- Easier withdrawal processing

- Improved online services

What Does EPF Scheme 2026 Mean for Employees?

The introduction of EPF Scheme 2026 primarily modernizes the provident fund system under the Code on Social Security, 2020 without disrupting existing member benefits.

Key highlights include:

- Existing EPF membership continues automatically.

- Current PF balances remain fully protected.

- Mandatory contribution rules remain unchanged.

- Greater flexibility for voluntary contributions.

- Continued access to partial withdrawals for eligible purposes.

- Stronger safeguards for contract workers.

- Increased focus on digital documentation and service delivery.

Overall, the new scheme aims to simplify provident fund administration while providing employees with greater flexibility and improved access to social security benefits. Existing subscribers can continue using their EPF accounts as before while taking advantage of the procedural improvements introduced under the updated framework.