When it comes to building wealth, consistency matters—but so does choosing the right investment avenue. If you invest ₹50,000 every month for 10 years, the difference between a safe option and a growth-oriented strategy can be massive. The big question investors often face is: should you rely on the stability of a Public Provident Fund (PPF) or take the market-linked route through a Systematic Investment Plan (SIP)?

Let’s break it down in a simple and practical way.

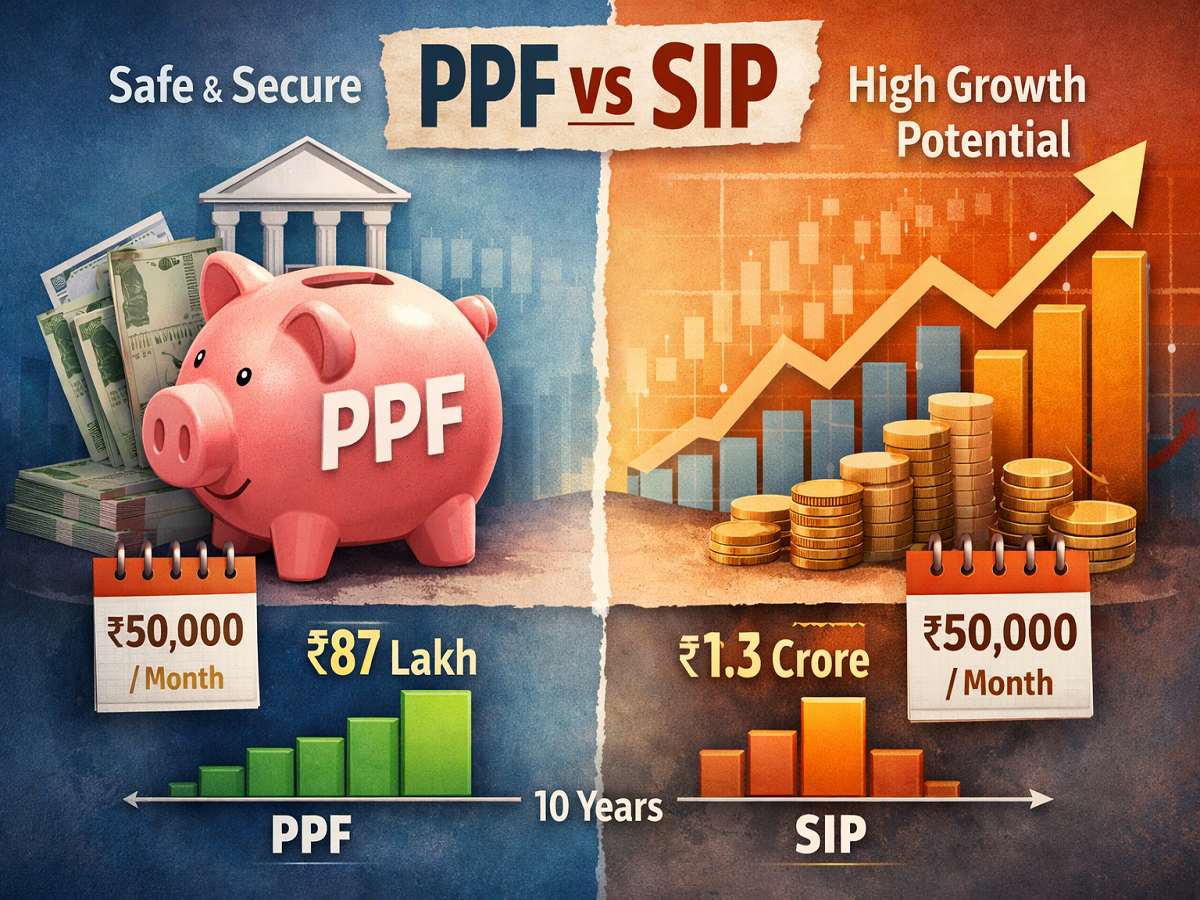

Growth vs Stability: The Core Difference

A Systematic Investment Plan (SIP) primarily invests in equity mutual funds, which are linked to stock market performance. Over the long term, SIPs have the potential to generate annual returns of 12% to 15%, depending on market conditions.

On the other hand, Public Provident Fund (PPF) offers a fixed interest rate of around 7.1%, backed by the government. It ensures capital safety and predictable returns.

What does this mean for your ₹50,000 monthly investment?

- SIP (12–15% returns): ₹1.15 crore to ₹1.3 crore in 10 years

- PPF (7.1% returns): Around ₹87 lakh in 10 years

Clearly, SIPs have the edge in terms of wealth creation—but they come with risk.

Returns Are Not Guaranteed in SIP

Unlike PPF, SIP returns are not fixed. Market fluctuations can impact short-term performance. However, over a longer horizon like 10 years, equity investments have historically outperformed traditional instruments.

The key is discipline. Staying invested during market ups and downs helps investors benefit from long-term compounding.

Safety and Tax Benefits: PPF’s Stronghold

PPF remains one of the safest investment options in India. It offers:

- Government-backed security

- Guaranteed returns

- Completely tax-free maturity (EEE status)

For conservative investors or those in higher tax brackets, PPF becomes a reliable choice. It provides peace of mind, even if returns are relatively lower.

The Impact of Inflation

Inflation silently reduces the real value of your money.

- PPF at 7.1% with 5–6% inflation = real return of just 1–2%

- SIP at 12–15% = real return of 6–9% (after inflation)

This is why SIPs are often preferred for long-term wealth creation—they help your money grow faster than inflation.

Investment Limits You Should Know

One major limitation of PPF is its annual cap:

- Maximum investment: ₹1.5 lakh per year (₹12,500 per month)

So, if you plan to invest ₹50,000 monthly, only a portion can go into PPF. The remaining amount must be invested elsewhere—making SIP a natural choice.

Market Volatility: Risk or Opportunity?

Many investors fear market ups and downs. However, SIPs turn volatility into an advantage through rupee cost averaging:

- You buy more units when prices are low

- You buy fewer units when prices are high

- Over time, this reduces the average cost

This strategy can significantly improve long-term returns—provided you stay invested and avoid panic selling.

What Should You Choose?

There is no universal answer—it depends on your financial goals and risk appetite.

Choose PPF if:

- You prefer safety over high returns

- You want tax-free, guaranteed income

- You have low risk tolerance

Choose SIP if:

- You aim for higher long-term wealth

- You can handle market fluctuations

- You have a long investment horizon

The Smart Strategy: Combine Both

Instead of choosing one over the other, financial experts often recommend a balanced approach:

- Use PPF for stability and tax benefits

- Use SIP for growth and wealth creation

This combination helps you reduce risk while maximizing returns over time.

A monthly investment of ₹50,000 can grow into a substantial corpus over 10 years—but the outcome depends on where you invest. While PPF offers security, SIPs provide growth potential.

The smartest move is not about picking a winner—it’s about building a strategy that aligns with your goals, risk profile, and future needs.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Always consult a certified financial advisor before making investment decisions.