NEWS

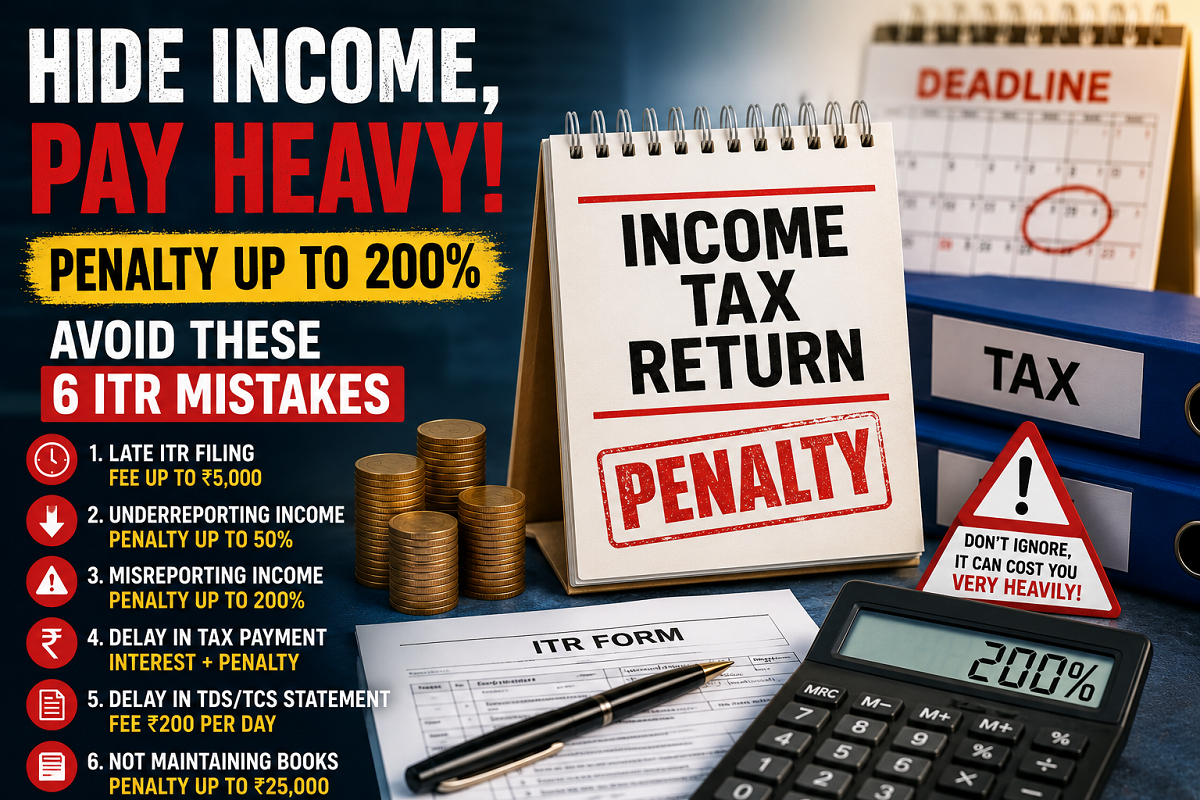

ITR Filing Mistakes Can Cost You Dear! Avoid These 6 Errors to Stay Away From Penalties Up to 200%

Late ITR Filing, Hidden Income, or Incorrect Tax Details Could Lead to Heavy Penalties Under the Income Tax Act

Filing your Income Tax Return (ITR) accurately and on time is essential to avoid unnecessary financial penalties. Many taxpayers assume that submitting the return before the deadline is enough, but even small errors—such as omitting income sources, underreporting earnings, or failing to maintain required records—can result in significant fines, interest charges, and legal complications.

According to the provisions of the Income Tax Act, different types of non-compliance attract different penalties. In certain cases involving incorrect reporting of income, taxpayers may even face a penalty of up to 200% of the tax payable on the misreported income.

Here are six common ITR filing mistakes that every taxpayer should avoid.

1. Missing the ITR Filing Deadline Can Attract a Late Fee

One of the most common mistakes is filing the Income Tax Return after the prescribed due date.

Under Section 234F of the Income Tax Act, taxpayers who fail to submit their return within the specified timeline may have to pay a late filing fee of up to ₹5,000.

However, individuals whose total taxable income does not exceed ₹5 lakh are eligible for a reduced late filing fee of up to ₹1,000. Filing the return on time not only avoids penalties but also ensures smoother processing of refunds and other tax-related benefits.

2. Underreporting Income May Lead to a 50% Penalty

Taxpayers must disclose income from all sources, including salary, business income, rental income, interest, capital gains, and other taxable earnings.

If the tax authorities determine that a taxpayer has underreported income, Section 270A allows for a penalty equal to 50% of the tax payable on the underreported amount.

Such situations may arise if income is unintentionally omitted or reported incorrectly while filing the return.

3. Misreporting Income Could Result in a 200% Penalty

The consequences become much more serious if the tax department concludes that the incorrect disclosure amounts to misreporting rather than a genuine error.

Misreporting may include:

- Concealing taxable income.

- Providing false financial information.

- Claiming deductions without valid evidence.

- Making incorrect entries in financial records.

In such cases, the penalty can rise to 200% of the tax payable on the misreported income under the applicable provisions of the Income Tax Act.

4. Delay in Paying Tax Can Also Invite Penalties

Submitting the return alone does not complete tax compliance. Taxpayers are also required to pay any outstanding tax liability within the prescribed timelines.

Under Section 221(1), the Assessing Officer may impose a penalty if there is a default in tax payment. The penalty cannot exceed the amount of unpaid tax, but taxpayers may also be required to pay applicable interest along with the outstanding tax dues.

Timely payment helps prevent additional financial burdens and compliance issues.

5. Delay in Filing TDS or TCS Statements Can Be Expensive

Businesses and other entities responsible for filing Tax Deducted at Source (TDS) or Tax Collected at Source (TCS) statements must also adhere to statutory deadlines.

According to Section 234E, a delay in filing these statements can attract a fee of ₹200 per day until the statement is submitted.

The total fee, however, cannot exceed the amount of TDS or TCS involved in the respective statement.

6. Failure to Maintain Books of Account May Lead to a Fine

Certain taxpayers, particularly professionals and businesses, are legally required to maintain proper books of account and financial records.

If mandatory records are not maintained, Section 271A provides for a penalty of up to ₹25,000.

Proper documentation also becomes essential during tax assessments, audits, or verification proceedings.

Important Tips Before Filing Your ITR

To reduce the chances of receiving notices or penalties, taxpayers should ensure that:

- All sources of income are accurately disclosed.

- Bank interest, capital gains, and other taxable earnings are included.

- Tax liability is paid before filing the return, wherever applicable.

- Appropriate supporting documents and financial records are maintained.

- The correct ITR form is selected based on the taxpayer's income profile.

- The return is filed before the prescribed due date.

Final Takeaway

Accurate and timely ITR filing is more than just a legal requirement—it also helps taxpayers avoid unnecessary penalties, interest, and prolonged disputes with tax authorities.

Whether it is reporting complete income, paying taxes on time, maintaining proper records, or filing mandatory statements within the deadline, following the prescribed tax rules can save taxpayers from significant financial consequences. Reviewing every detail carefully before submitting the return remains one of the best ways to ensure hassle-free tax compliance.