NEWS

ITR Filing 2026: Earning Above ₹1 Crore? Don’t Skip This Mandatory Schedule or You May Receive a Tax Notice

Taxpayers With Annual Income Exceeding ₹1 Crore Must Disclose Assets and Liabilities While Filing ITR

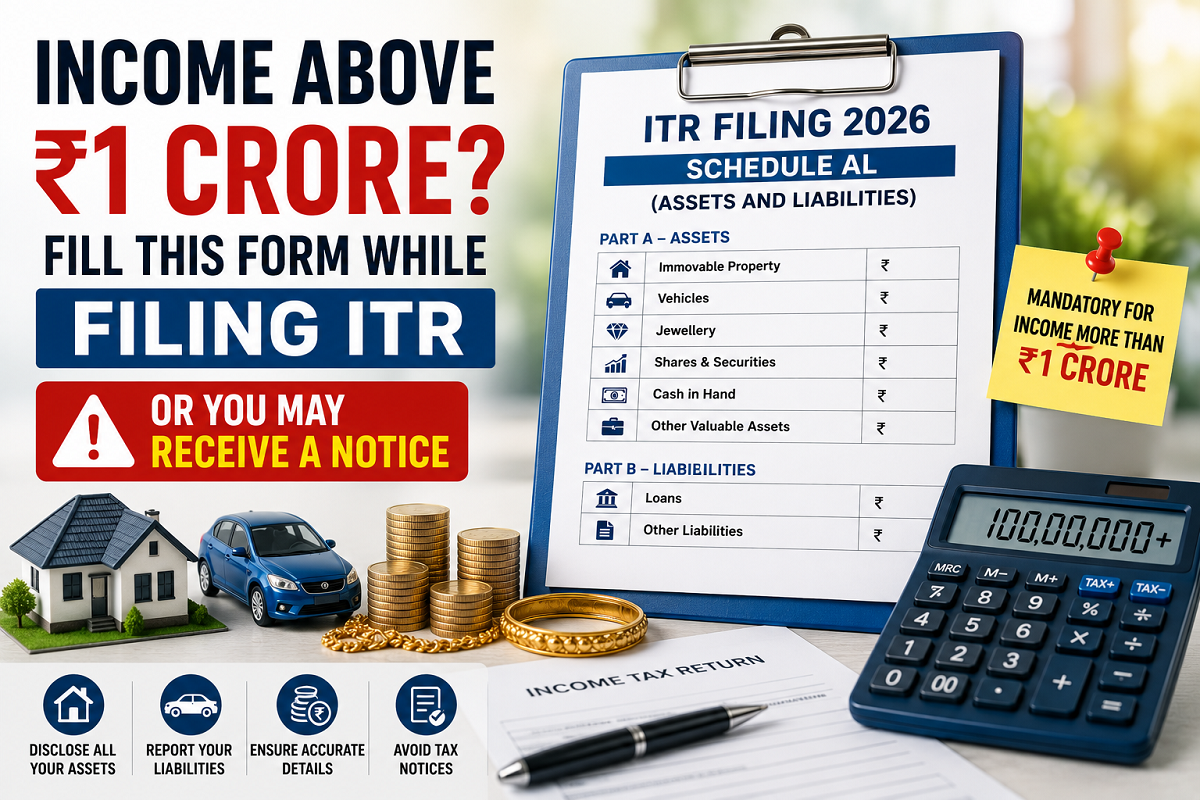

Individuals and Hindu Undivided Families (HUFs) whose total income exceeded ₹1 crore during Financial Year 2025–26 need to pay special attention while filing their Income Tax Return (ITR). Apart from reporting income, they are also required to submit detailed information about their assets and liabilities by filling Schedule AL (Assets and Liabilities).

The Income Tax Department has made this disclosure mandatory for eligible taxpayers filing ITR-2 or ITR-3. Failure to provide complete or accurate information may increase the chances of receiving a notice or query from the tax authorities.

What Is Schedule AL?

Schedule AL, short for Assets and Liabilities, is an additional section in the Income Tax Return designed to collect information about a taxpayer's financial holdings and outstanding liabilities.

This requirement applies to:

- Individual taxpayers whose total income exceeds ₹1 crore during FY 2025–26.

- Hindu Undivided Families (HUFs) crossing the same income threshold.

Taxpayers filing ITR-2 and ITR-3 within this income category are required to complete this schedule. Companies have separate reporting requirements under ITR-6, which includes dedicated schedules for asset disclosures.

Which Assets Must Be Reported?

Schedule AL requires taxpayers to disclose the value of major assets owned as of March 31, 2026.

The information generally includes:

- Residential and commercial properties.

- Land and other immovable assets.

- Motor vehicles.

- Gold, jewellery, and precious ornaments.

- Shares, securities, and investments.

- Cash held in hand.

- Valuable collectibles and other significant assets.

In addition to assets, taxpayers must also report liabilities directly linked to those assets, such as outstanding loans or borrowings.

How Should Asset Values Be Declared?

According to the Income Tax Department's guidelines, assets should generally be reported based on their original purchase cost rather than their current market value.

If additional expenditure has been incurred for renovation or improvement, those costs may also be included where applicable.

For assets received through:

- Gift

- Inheritance

- Will

- Family transfer

the value can be reported based on the previous owner's acquisition cost along with eligible improvement expenses.

Where historical purchase details are unavailable, taxpayers may provide a reasonable estimated value based on available records.

Why Has This Disclosure Become Important?

The Income Tax Department has observed instances where a taxpayer's declared income did not appear consistent with the value of assets owned.

By requiring high-income taxpayers to submit Schedule AL, the department aims to:

- Improve transparency in tax reporting.

- Compare asset ownership with declared income.

- Detect possible tax evasion or undisclosed wealth.

- Strengthen compliance among high-income individuals.

The disclosure is intended to assist tax authorities in verifying whether a taxpayer's financial profile aligns with the income reported in the return.

Points Taxpayers Should Remember

Before submitting the return, eligible taxpayers should ensure that:

- Asset and liability details reflect their position as on March 31, 2026.

- Information provided is complete and accurate.

- Supporting financial records are available in case of future verification.

- Liabilities connected with disclosed assets are correctly reported.

For Non-Resident (NR) and Resident but Not Ordinarily Resident (RNOR) taxpayers, only assets located within India are generally required to be disclosed under the applicable rules.

Avoid Errors While Filing Your Return

Providing incomplete or incorrect information in Schedule AL may result in additional scrutiny from the Income Tax Department. Tax experts recommend carefully reviewing asset details before filing the return and maintaining supporting documents wherever possible.

As income tax compliance becomes increasingly data-driven, accurate reporting of both income and assets is essential for avoiding unnecessary notices and ensuring smooth processing of the return.

Taxpayers whose annual income exceeds ₹1 crore should therefore treat Schedule AL as an important part of the ITR filing process rather than an optional disclosure. Proper compliance can help reduce the risk of future tax-related queries and promote transparent financial reporting.